On conflicted capital, mind games, and untapped opportunity

It’s been almost a year since I wrote “Two Worlds of Venture” on the growing gap between founders who are able to raise millions of dollars seemingly overnight and those who struggle to raise any amount at all. I ended that blog with the following:

“Ultimately, the data will show if we’re making any meaningful progress. If 2020 was any indication, in times of uncertainty, VCs double down on their existing networks rather than expanding their reach. We have 9 months left in 2021 to move forward instead.”

Now that 2021 is behind us, the results are clear: not only did we not move forward, we actually moved backward in many ways. Here are my observations of venture capital’s evolution over the past year:

The funding gap has widened. There has been a more extreme consolidation of capital at both the fund & startup level, as the increases in dollars allocated to funds and startups have outpaced the increases in the numbers of funds and deals.

Becoming a VC is easier, but staying one is harder. While the barrier to entry for first-time funds has never been lower thanks to tech-enabled back office infrastructure and regulatory changes, the institutionalization of new firms remains a challenge, as many established institutional LPs structurally lack the appetite to add new managers to their portfolios.

Everyone’s fingers are in everyone’s pies. Emerging fund managers are increasingly raising capital from larger, more established venture funds, even in cases where the latter have directly competitive investment strategies themselves.

This continued concentration, combined with increasing comingling of investment entities that arguably should remain independent, creates a perfect storm of conflicts of interest, misaligned incentives, missed opportunities, and compression of returns across the entire venture asset class. For founders, emerging fund managers, and LPs alike, this dynamic presents existential risk. At the same time, there is a wide open field for investors to win by averting this structural gridlock. Let’s dig in 👀

The funding gap has widened

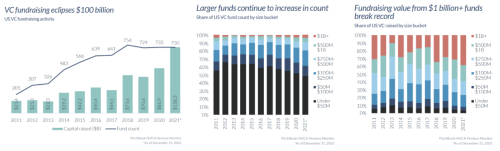

First up: investment activity into startups. Based on the Q4 Venture Monitor (Pitchbook, NVCA Insperity), dollars invested into startups grew 98% year-over-year in 2021, while unique deals counts only grew an estimated 40%.

This report tells a similar story about early stage investment activity specifically: dollars invested grew over 50% year-over-year, but deal counts only grew an estimated 25%. If you take a longer-term view, the contrast is even starker: over a 10-year period, dollars invested grew over 600%; while deal count only grew an estimated 150%.

You might be wondering how this is possible given that everyone and their mother seems to have a fund now, and dozens of articles claim that “record-breaking” amounts of capital have been raised by venture funds. Shouldn’t more checkwriters result in more checks being written?

Unfortunately, the trend at the fund level is consistent with that at the startup level: while invested dollar amounts have grown, that growth is concentrated in later stages, larger funds, and, ultimately, fewer funds overall.

The data tells a very clear story about what is happening, but it doesn’t tell us much about why. In an industry premised on power laws, probabilistic models, and outlier outcomes, why aren’t we trending toward greater structural diversification?

The answer lies in the financial structures and decision-making processes of funds and institutional LPs. Grab a cup of coffee, this next part is dense 😬

Becoming a VC is easier, but staying one is harder

If you’re a founder who has raised venture capital, you’ve probably heard a laundry list of reasons why certain investors won’t cut you a check. These constraints – investment scope (“we only invest at seed, not Series A”; “we only invest in fintech”), check size (“we can’t invest in a round this small because our minimum check size is $5 million”) and ownership targets (“we are aiming for 10% fully-diluted ownership) – may seem arbitrary. Fund managers generally select these criteria based on the perceived potential to generate outsized returns, but their decisions are also informed by concrete logistical constraints.

For one, fund managers make money in two main ways: management fees, based on assets under management (AUM), charged annually over the duration of a fund’s life (typically 10 years), and carried interest, which is effectively a percentage of the fund’s profits. This dual business model creates a tension between maintaining disciplined fund sizes (extensive data shows that return multiples decline as fund size increases) and increasing assets under management (to increase management fees). VCs have limited bandwidth and resources to find, select, and support portfolio companies, particularly given their fixed timelines to deploy capital, meet performance expectations (such as portfolio mark-ups), and raise additional funds. As emerging VCs search for ways to “differentiate” themselves and elevate their brands, they sometimes chase “hot deals” with “marquee” co-investors, particularly since LPs place weight on these industry relationships in their decision-making.

The end result? Bigger checks, higher valuations, more risk, less upside, and – to bring it full circle – fewer companies funded.

At the GP/LP fundraising level, the market of existing institutional investors is even more consolidated. The institutional investors that traditionally back venture funds include university endowments and foundations (with hundreds of millions or a few billion dollars in AUM), large corporations (often investing from balance sheet capital), pension funds (tens of billions of dollars in AUM), and sovereign wealth funds (hundreds of billions of dollars in AUM). LPs typically advise new VCs to raise a small proof-of-concept fund (often from non-institutional investors, such as high net worth individuals), demonstrate early results, and then approach institutions for their next (larger) fund.

While this advice may sound logical, the reality is that many of the institutions that have historically backed early stage venture funds are at capacity for investing in new managers. Part of this is a function of macroeconomic conditions, and part of it is by design. Just as VCs construct their portfolios based on check size, number of companies, and investment pace, LPs similarly consider their allocation per asset class and individual manager. They often have relatively small investment teams, so they have extremely limited capacity for sourcing, diligence, and monitoring of managers in an asset class that ultimately represents a very small sliver of their total AUM.

Given these constraints, many LPs prefer to keep investing larger amounts into the same firms rather than adding new ones. This long-term commitment to existing managers is so strong that it often extends across different fund strategies. Whether it’s because they believe that one of their current early stage managers is the best choice for a new strategy, or because they are obligated to back the firm’s new fund to secure their allocation in the firm’s next core fund, LPs are strongly inclined to back the same firm’s growth fund (or India-focused fund, or healthcare-focused fund) over a different manager’s, thus driving up the AUM of a limited number of firms at the expense of newer managers’ growth. In the rare case that LPs do have capacity or interest in adding a new manager, they rely heavily on recommendations, references, and endorsements from managers they have already backed, keeping capital perpetually consolidated within a fairly tightly knit ecosystem. It is no coincidence that the majority of new fund managers that have reached scale (i.e. less than 10 years old with hundreds of millions of dollars in AUM) were either spun out of or anchored by established venture franchises.

These dynamics have created a flywheel in which LPs commit to funds with the expectation of continuing and increasing their investments into them over time, driving VCs to raise larger funds. Because of the market pressures to deploy said capital, VCs write larger checks & increase deployment pace, and because of increases in valuations and round sizes, VCs raise even larger funds. And so on, and so on. While everyone points their fingers at various “market forces”, you can’t help but feel like everyone’s in on a scheme that’s working exactly as designed.

If you are in favor of innovation, free markets, and competition, all of the above should be unsettling. You could argue that venture capital is following the same “professionalization” that other sectors of financial services have experienced, but that doesn’t make it any less concerning. After all, venture capital’s purpose is to generate outsized returns by identifying outliers, and in its current form, it is fundamentally about discretion. Having fewer decision-makers means that founders working on under-appreciated or unfamiliar ideas have lower odds of getting funded, resulting in an immeasurable loss of both financial returns and innovation.

Everyone’s fingers are in everyone’s pies

This concentration of decision-makers is troubling enough, but something even more concerning is happening: an enmeshment of venture capital.

Enmeshment is “a description of a relationship between two or more people in which personal boundaries are permeable and unclear”. This term is used predominantly in psychology and interpersonal relationships, but it is also an apt descriptor for the financial entanglement occurring in venture capital.

We are increasingly seeing venture capital firms, particularly established franchises with tens of billions of dollars of AUM, investing in smaller, newer firms as LPs. In many cases, the VC firms acting as LPs are executing on the same or similar investment strategies as the VC firms they invest in. Established funds anchoring new ones isn’t a new phenomenon, but as this practice has accelerated, the conflicts have become clearer.

A few recent examples:

Bain Capital Ventures, which “raised $1.3 billion to fund young startups and young VC, firms, too” has reportedly already backed 50 emerging managers

Seven Seven Six, a pre-seed and seed stage-focused venture capital firm, announces they will be seeding micro funds

Founders Fund, a stage-agnostic venture capital firm that also sometimes incubates startups, led a $20M Series A in On Deck, a company that runs numerous fellowships as well as a startup accelerator that structurally seems similar to YC. On Deck’s founder & co-CEO is also a co-founder and partner at Village Global, a different $100 million venture capital fund

Tiger Global’s partners committed $1 billion to fund early stage tech funds while Tiger, as a fund, focuses on private investments as early as seed (this is not the same as Tiger’s fund investing as an LP in other funds, which it may also be doing, but it’s worth mentioning given the sheer magnitude of the commitment)

Sequoia and Andreessen Horowitz, stage-agnostic venture capital firms with dedicated seed funds, invested $23M in a holding company that holds Product Hunt, a leading startup product discovery platform, and another early stage venture fund 🤔 (I can’t be the only one scratching my head at this one)

Look at the LP list of any emerging fund over $25M from the past year, and you will almost certainly see a big fund named. Many, many more such deals are happening under the radar, including anchor checks of hundreds of millions of dollars.

There’s a bit of an “everything old is new again” feeling here. In 2014, Y Combinator announced that in order to “reduc[e] conflicts”, they had ended all “LP and LP-like … relationships with several VC firms”. I don’t know if YC’s LP base still excludes VCs, but this decision is one of few public acknowledgments I’ve seen of the fraught nature of these relationships.

While hybrid investment strategies are not new in and of themselves, institutions typically do not directly compete against the funds they back. They also generally have clear policies on conflicts of interest, separate teams for fund investments vs direct investments into companies, and limited-to-no influence in the funding dynamics between venture funds and the startups they back. As the lines between stakeholders increasingly blur, the enmeshment of venture capital becomes harder to deny.

Given the structural constraints that new managers face when raising from institutional LPs, it comes as no surprise that emerging fund managers are seeking alternative capital sources, including from other funds. Plus, the benefits of this kind of arrangement are tempting:

Faster time to market: why spend two years raising $10M when you could raise $25M in one?

Tangible value prop to founders: “we have a close relationship with Brand Name Fund and can help you raise a larger next round”

A coveted endorsement: having a stamp of approval from one of The Chosen Ones elevates your fund’s brand and profile and allegedly makes your future fundraising from institutional LPs easier

But for new fund managers looking to build a long-lasting firm, this type of relationship is akin to winning the battle but losing the war. Especially if decision-makers are not clearly delineated and conflicts of interest are not transparently addressed, emerging fund managers who accept LP capital from larger funds are:

Strengthening incumbents' positions as arbiters of innovation capital. These large funds have a vested interest in controlling distribution, and favoring them distorts capital flows into the startup layer and risks emerging funds’ future market leadership potential.

Boosting the returns and accelerating the financial prominence of established VCs. Sure, the paltry check they write into any individual fund is a rounding error for their overall AUM, but given they’re backing many managers, the returns can be meaningful in the aggregate. We still believe emerging funds have the potential to deliver 5-10x+ net to LPs, don’t we?

Compromising their own independence and their portfolio companies’ optionality, potentially to the detriment of returns. In Mario Gabriele’s piece “The Future of Solo Capitalists”, he quotes the former manager of a large fund: “Many [solo GPs] I’ve backed have taken large LP checks from a16z, Thrive, TPG and others. Those funds tend to get exclusive rights to pro-rata and follow on rounds…again this will knee cap returns. It is certainly appealing to get that money in the door but it limits future growth and ability to show institutional LPs a track record worthy of a bigger fund II.” Agreements favoring some later stage investors over others also create another layer of incentive misalignment between VCs and founders. Even if there are no binding terms regarding the emerging manager’s strategy and the relationship with the portfolio companies, it is impossible to completely disregard the interests of these LPs, especially given the strategic importance of their ongoing endorsements and references.

Further choking out institutional appetite to allocate to emerging managers and reducing independent sources of capital for new funds in the future. The risks here are multiple. For one, the larger fund that put a new one in business may expand its own direct investment strategy in a way that cannibalizes them. Additionally, institutional LPs will be less motivated to invest in emerging managers directly if they receive sufficient exposure to them through their existing fund investments. Over time, this trends toward even greater consolidation and lower industry-wide returns, as established VC firms have neither the objectivity nor the incentive to fund the highest potential managers. After all, if you were an established market leader, would you elevate someone who you thought could beat you at your own game? At scale, this reduction in uncompromised, independent LP capital sources leaves emerging managers at the mercy of their larger, better funded competitors in perpetuity.

The notion that established venture capitalists could be reliable judges of future VC industry leaders under any circumstances is suspect, particularly given VCs' shortcomings and deeply entrenched biases. Diversity in funding outcomes is the canary in the coal mine: it doesn't guarantee optimal performance, but the homogeneity we've seen to date guarantees the lack thereof. Over-reliance on incumbents has resulted in not only broad financial inefficiency but also stunning lapses in judgment. We witnessed LPs committing $300M to a new venture firm based on the founding partners’ Tier 1 VC track records and glowing endorsements, only to later discover that there were reports of sexual harassment allegations against one of the partners at three of his prior firms that no one told them about. In another instance, we saw LPs increase their commitment to a $5B+ Tier 1 VC firm with $560M of fresh capital for a new fund with no women or Black/Latinx investors on their 7-person investment team (yes, in 2022).

Even initiatives explicitly aiming to fix venture capital’s diversity issues rely on existing managers for new manager selection. Screendoor is “a coalition of experienced venture capitalists, institutional investors, and seasoned operators”. Their first investment vehicle is an $87 million fund, raised mostly from more than a dozen large institutions with over $200 billion in collective AUM. According to Screendoor’s FAQ, investment decisions are made by an Investment Committee composed of both venture capitalists and institutional investors. None of the affiliated venture capital firms are LPs in Screendoor, though all of the Founding Advisors (i.e. the individual venture capitalists) have reportedly invested personally. The cynical view is that this feel-good initiative lets large LPs off the hook without moving the needle; a press release that institutions have committed 0.04% of their AUM to diverse emerging VC managers is only inspiring if you don’t do the math. The ambitious interpretation is fraught with conflict: if this is the first step in a meaningful shift toward institutional capital allocation into new VC entrants, why are other VCs whom they’d potentially displace involved?

Despite all these reservations, I'm willing to suspend my disbelief and entertain the idea that involving existing VCs in the selection process for new VCs could have any merit. In such a scenario, what would be the best practices for structuring these relationships at scale? What are the mechanisms for transparency, governance, and accountability that ensure that conflicts of interest are adequately mitigated, independence is maintained, and capital is deployed efficiently? Absent progress in these areas, the increased enmeshment is sure to result in continued suboptimal outcomes, including lower returns and a decline in innovation.

The more time I spend peeling back the onion, the more questions I have. Maybe you can help me unravel some of them.

If you are a founder:

Do you know who your investors’ investors are? Do you ask? Do you care?

Does it concern you that this trend may decrease competitiveness among VCs during your fundraising processes and potentially impact your valuation, dilution, and future optionality?

Are you concerned with information flows, signaling risk, and your VCs’ ability to provide objective guidance if their financial incentives are intertwined with other VCs’?

If you are an LP:

How do you account for the reduction in competitive forces and the impact on asset class-wide returns as the financial incentives of funds become increasingly co-dependent?

How do you evaluate references from investors who are financially aligned with and potentially under non-disparagement agreements with one another? How does this enmeshment change your due diligence processes?

Do you believe that fund managers who are either unknown to or perhaps even disfavored by incumbents have the potential to generate outsized returns? If not, why not? If so, what are your mechanisms for sourcing, evaluating, and selecting such managers?

And, finally, if you are an aspiring venture capital fund manager:

How are you planning to build a sustainable capital base in what is largely a captive market?

Is independence important to you?

What do you know for certain about the venture capital industry, and what do you doubt?

As a chunk of the existing market ends up stuck in this web, there’s a wide open field for anyone who sees the potential of bucking the trend. Building a new structure is the most exciting opportunity we have. If you have any thoughts, feedback, or ideas, I’m at geri [at] laconia [dot] vc and @geri_kirilova on Twitter.

Thank you to Doba Parushev, Halle Kaplan-Allen, Frank Brown, Rich Cooksen, and my Laconia teammates for their thoughtful feedback on this piece and Del Johnson for countless conversations on this topic.